In a world already stretched thin on refined fuels, diesel has emerged as the undisputed king of commodities—and refineries are proving to be the fragile link in the global supply chain. As of early April 2026, the ongoing disruption in the Strait of Hormuz—triggered by the Iran conflict—has created the largest supply shock in diesel markets in history, according to the International Energy Agency (IEA).

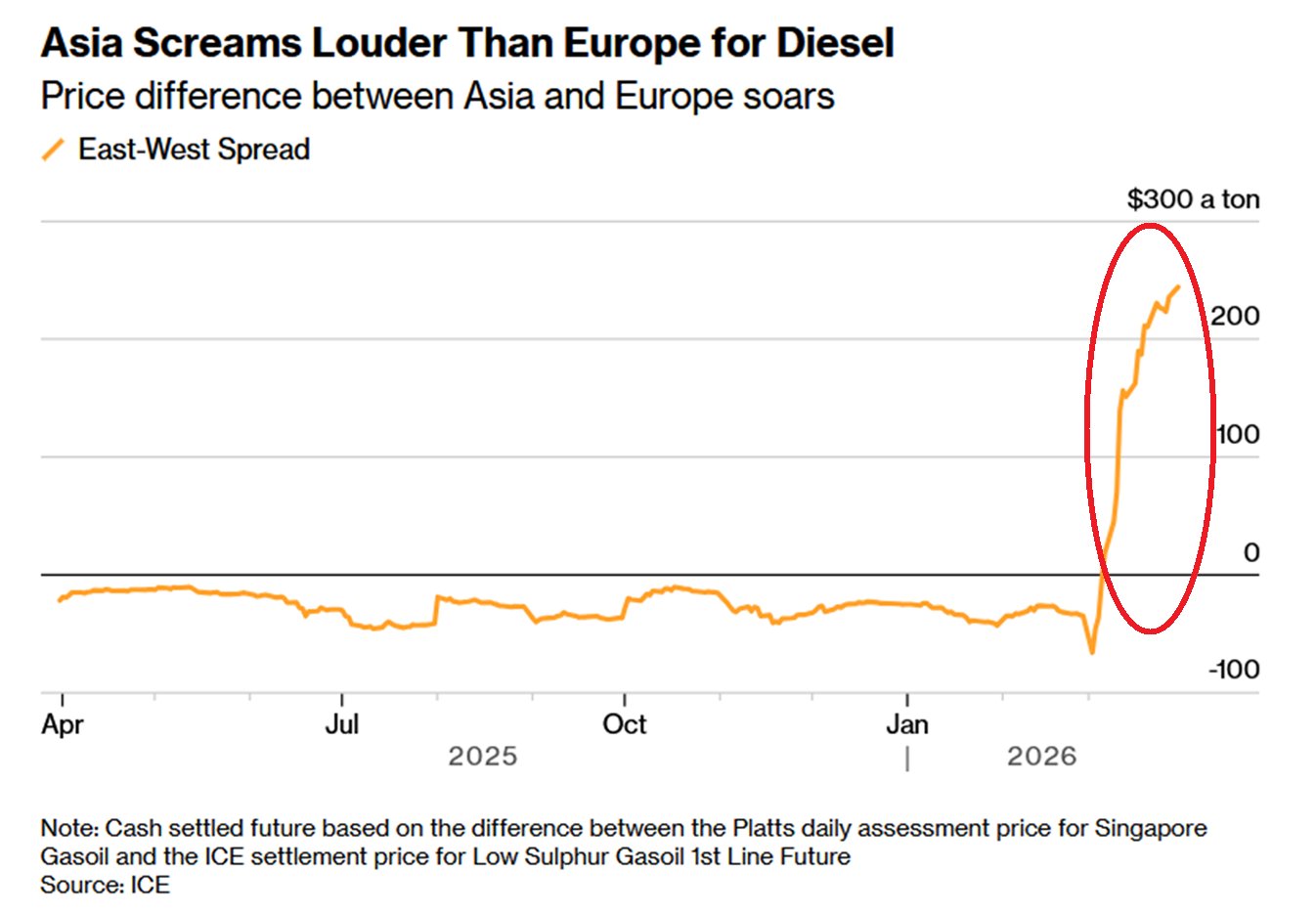

A viral analysis from Global Markets Investor (@GlobalMktObserv) on X captured the chaos perfectly: Asian diesel shortages have grown so acute that traders are shipping fuel from the UK and U.S. West Coast halfway around the world. The price spread between Asian and European diesel exploded to $244 per ton (up from near zero pre-crisis), making 12,000-mile voyages from the UK to Australia and U.S. cargoes to Singapore and Pakistan suddenly profitable. Europe itself is diesel-short, yet barrels are being diverted to Asia because the situation there is even more dire. The longer the Strait remains closed or restricted, the fiercer the global scramble for every available barrel of middle distillate will become.

This isn’t just a Middle East story. It’s exposing deep structural weaknesses in global refining capacity, regional dependencies, and the razor-thin margins that keep diesel flowing. Here’s a breakdown of the weak points, the regional flashpoints, and what it means for U.S. investors and everyday consumers.

Global Diesel Markets: Refineries as the BottleneckDiesel (and other middle distillates) production relies on complex refineries that crack crude into usable fuels. But global refining capacity has been shrinking for years due to:

Permanent closures and conversions: Roughly 1 million barrels per day (b/d) of capacity in Europe and the U.S. is slated for shutdown or conversion to renewable diesel in 2025-2026, driven by weak margins, environmental regulations, and the shift to lower-carbon fuels.

Maintenance outages and unplanned disruptions: Russian refinery attacks, U.S. winter storms, and routine turnarounds have kept utilization rates high (often 90%+ in key hubs) while inventories remain critically low—U.S. distillate stocks started 2026 below the 10-year average and are projected to tighten further.

Geopolitical chokepoints: The Strait of Hormuz normally carries ~20% of global oil and a massive share of refined products to Asia. Its effective closure has slashed 3-4 million b/d of diesel-related flows, plus another ~500,000 b/d from Middle East refinery exports.

The result? Refining margins (crack spreads) have soared—diesel cracks in some regions hitting $44–$50 per barrel—turning refiners into the big winners while consumers and downstream industries pay the price.

Regional Weak Spots Highlighted by Hormuz

Asia: Ground Zero for the Crisis

84% of crude (and a huge share of products) transits Hormuz heads to Asia. China has banned diesel, gasoline, and jet fuel exports until at least the end of March to protect domestic supply. Southeast Asia is scrambling, with countries like Thailand imposing price caps and urging conservation. Traders are pulling barrels from Europe and the U.S. just to keep factories and trucks moving.

Australia: Mining on the Brink

Up to 40% of Australia’s diesel is consumed by mining operations, powering over 50,000 large trucks. With the traditional Middle East supply cut off, tankers from the UK are now making uneconomic 12,000-mile runs. Any prolonged shortage threatens mining output, which ripples into global commodity prices for metals and minerals.

California (and the U.S. West Coast): Next in Line

California is the most exposed U.S. region—an “energy island” with no easy pipeline access to domestic crude and heavy historical reliance on Middle East imports via Hormuz. Two major refinery closures (Phillips 66’s Los Angeles complex in late 2025 and Valero’s Benicia refinery in April 2026) have removed ~8–10% of state capacity at the worst possible time. Diesel prices have already smashed records above $5–$6/gallon nationally, with California seeing even steeper spikes; worst-case scenarios warn of $7–$10/gallon fuel and outright shortages. Chevron has publicly warned of an impending crisis unless regulations ease.

The U.S. as a whole isn’t immune—diesel futures have surged faster than crude or gasoline, pushing national averages over $5/gallon for the first time since 2022 and threatening trucking, agriculture, and freight costs.

What U.S. Investors Should Watch

Refiners are the clear bright spot. High crack spreads have already delivered banner returns for major players:Valero Energy (VLO), Phillips 66 (PSX), and Marathon Petroleum (MPC) posted 25–28% YTD gains early in 2026 as margins doubled or tripled in some quarters. UBS and Goldman Sachs have raised 2026 margin forecasts sharply, with U.S. composite cracks now eyed at $26+/barrel.

Key signals to monitor:

Weekly EIA distillate inventory reports and refinery utilization rates.

Crack spread futures (especially ULSD vs. WTI).

Any signs of Hormuz reopening or coordinated SPR releases.

Downstream exposure: Companies with export terminals or renewable diesel capacity may hedge risks better.

Refining stocks could remain resilient even if crude prices moderate, as product tightness persists into 2027.

What Consumers Should Brace For

Diesel powers the economy’s backbone—trucks, farms, construction, and sand hauling. Higher costs are already rippling through:Freight and groceries: Every extra dollar on diesel adds surcharges that hit store shelves within weeks. Groceries, building materials, and consumer goods could see 5–10%+ price pressure if the crisis drags on.

Regional pain: California and the West Coast face the sharpest pump-price hikes and potential rationing signals.

Broader inflation: Trucking, agriculture, and manufacturing are diesel-intensive; expect second-order effects on everything from food to electronics.

Short-term relief could come from seasonal refinery restarts or global stock releases, but structural capacity losses mean volatility is the new normal.

- X Post (GlobalMktObserv): “The diesel shortage in Asia…” (April 2, 2026) – https://x.com/GlobalMktObserv/status/2039709941880001000

- IEA Oil Market Report (March 2026) and related commentary.

- Reuters, Bloomberg, Argus Media, Forbes, Newsweek, EIA Short-Term Energy Outlook (various 2025-2026 releases).

- Specific articles cited:

- https://www.newsweek.com/california-at-highest-risk-as-us-middle-eastern-oil-supply-dries-up-11767727

- https://theoregongroup.com/energy/strait-of-hormuz-diesel-shock-threatens-mining-industry/

- https://www.forbes.com/sites/rrapier/2026/03/03/the-california-energy-island-why-hormuz-hits-the-west-coast-hardest/

- https://finance.yahoo.com/news/global-market-fueling-inflation-fears-diesel-prices-surge-amid-strait-of-hormuz-tensions/articleshow/129437599.cms

- Goldman Sachs/UBS refining margin notes (Feb-Mar 2026).

- EIA refinery closure data: https://www.eia.gov/todayinenergy/detail.php?id=64644

Energy News Beat will continue monitoring this fast-moving situation. Diesel isn’t just a fuel—it’s the lifeblood of global trade, and the refineries that make it are under unprecedented strain. Stay tuned.