Energy News Beat Exclusive Analysis – Stu Turley

Diesel prices are surging across key markets—and rising faster than gasoline or petrol in many places. As Sky News economics editor Ed Conway highlighted in his widely shared X post and video primer (posted March 31, 2026), this isn’t just another blip in the energy markets. It’s the result of the worst global oil supply shock in modern history, compounded by decades-old policy decisions that left major economies structurally vulnerable.

What Ed Conway leaves out is how we got here. Look at California through government overreach and regulatory burdens we went from an estimated 39 refineries to 7, and 6 of those remaining refineries are slated to close due to CARB and regulatory burdens being forced on refineries. Stu Turley, David Blackmon, and Mike Akers will be covering this later this week on the Energy News beat podcast.

The trigger?

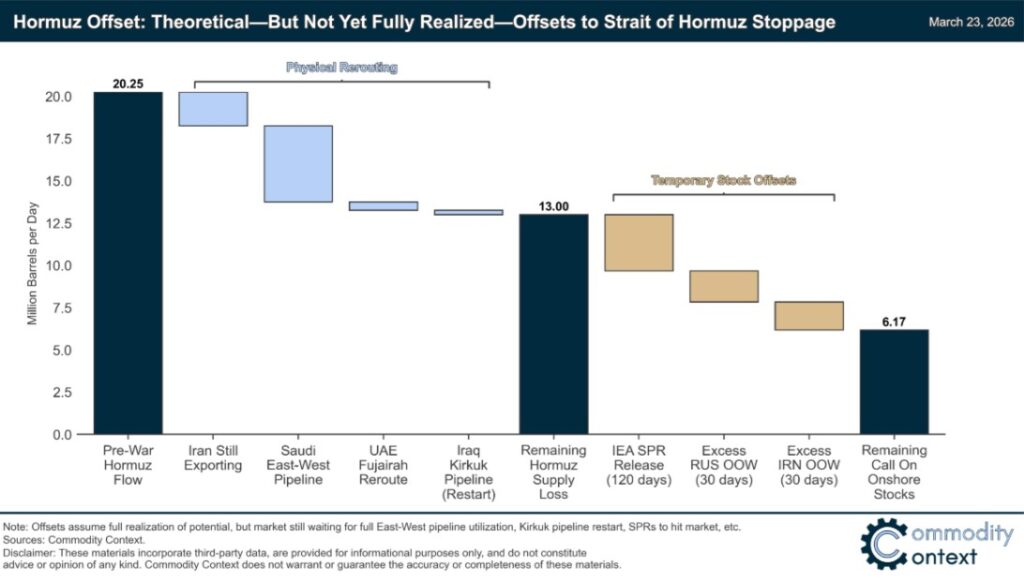

The ongoing US-Israel conflict with Iran has disrupted flows through the Strait of Hormuz and hammered Gulf oil infrastructure. Roughly 20 million barrels per day of crude and products once flowed through this chokepoint. Emergency rerouting via pipelines (Saudi East-West, UAE Fujairah) and stock releases have only partially offset the gap, leaving a persistent shortfall of several million barrels per day. Diesel (a middle distillate) is hit hardest because inventories were already tight heading into the crisis, and global refining is struggling to shift output quickly.

The UK: Diesel’s Perfect Storm of Policy and Refining Mismatch

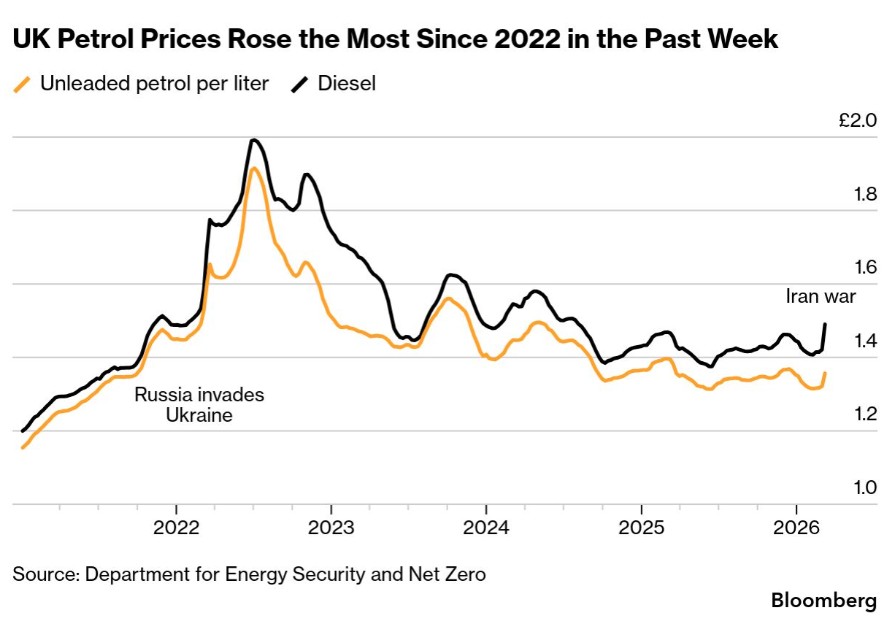

In the UK, diesel has jumped far faster than unleaded petrol—up roughly 28% in recent weeks versus ~15% for petrol, pushing averages to around 181p/litre for diesel (vs. ~152p for petrol).

Why? Go back to 2001–2002. Then-Chancellor Gordon Brown introduced vehicle excise duty (VED) incentives favoring lower-CO₂ diesel cars, sparking a “dash for diesel.” Diesel new-car registrations surged, peaking above petrol sales by 2015. The UK fleet shifted dramatically: today ~30–40% of vehicles (including HGVs) rely on diesel.

But UK refineries—many built in the 1960s–70s—were optimized for petrol output. Even when North Sea oil kept the country self-sufficient overall, diesel demand outstripped local production. Closures (down from ~10 major sites in 2009 to fewer today) worsened this. The UK now imports a large share of its diesel, much of it historically from Russia, then the Gulf, India, and Europe. Those Gulf-linked supplies are now disrupted.

Europe: Shared Vulnerability, Uneven Pain

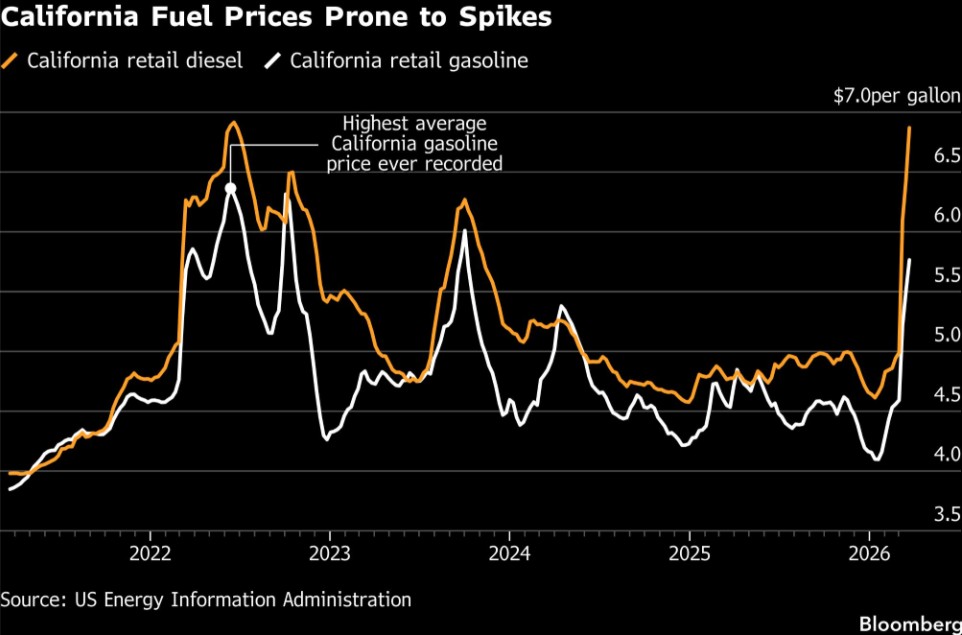

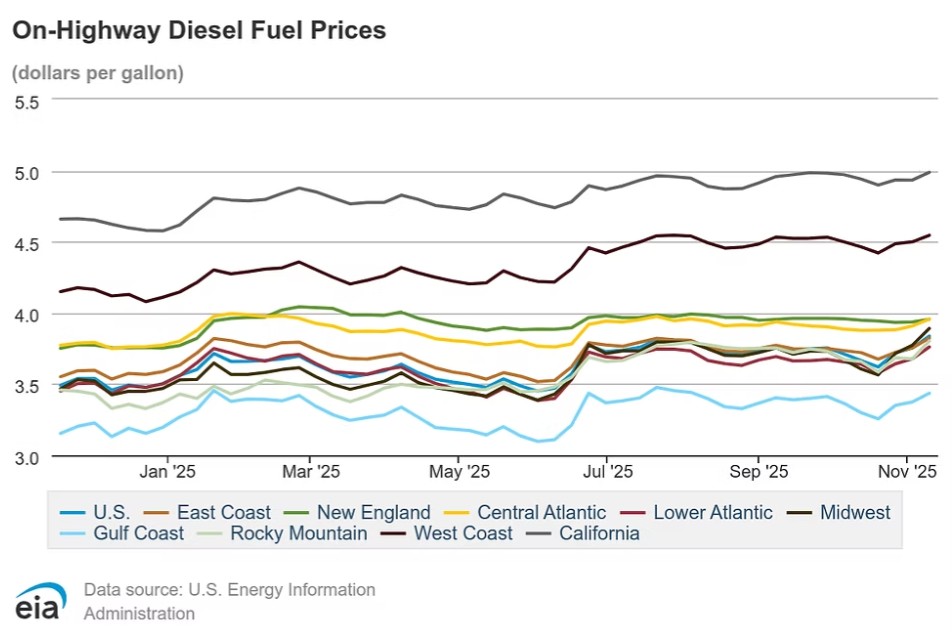

California and the West Coast: A Self-Made Fuel Island in Crisis

Across the Atlantic, California and the broader West Coast (PADD 5) are in the same boat—arguably worse. California diesel has hit records near $7/gallon in places, while gasoline tops $5.50–6/gallon. The state feels the global shock more acutely because of chronic local supply constraints.

Key factors:

Refinery closures: Phillips 66’s Los Angeles-area plant shut in late 2025; Valero’s Benicia facility is closing in April 2026. These represent ~17–20% of California’s refining capacity. West Coast capacity has steadily declined since 2017.

Unique fuel specs: California’s CARB-mandated cleaner blends (plus Low Carbon Fuel Standard) make the state a “fuel island”—imports from other US regions are difficult or impossible without reprocessing.

High taxes and regs: Combined state/federal taxes and compliance costs add over $1/gallon; the state is heavily reliant on imports (including ~30% from the volatile Middle East pre-crisis).

The result? When global crude cracks higher, California prices spike disproportionately. The West Coast as a whole shows diesel prices elevated versus the national average.

Why Diesel Specifically?

The “Crack Spread” Effect

Refiners earn more cracking crude into diesel right now because distillate inventories are tighter than gasoline (driven by trucking, heating oil overlap, and jet fuel competition). Geopolitics amplifies shipping/insurance costs for middle-distillate routes. In the UK/EU, import dependence on Gulf/Asian diesel magnifies the pain. In California, domestic capacity loss does the same.

Broader Impacts

Higher diesel means costlier freight, food, and goods. Trucking, logistics, agriculture, and construction feel it first. Inflation risks rise. EVs look more attractive in the long run, but the transition exposes vulnerabilities today.

For the UK, the EU, and California, it is also 100% faulty energy policies and following Net Zero without having a plan for Energy Security and Business Continuity.

Check out the Energy News Beat Substack: https://theenergynewsbeat.substack.com/

Appendix: Sources and Links

- Ed Conway Sky X post (March 31, 2026): https://x.com/EdConwaySky/status/2038869783567827176 (video primer on Gulf war economics and UK diesel history)

- Bloomberg UK fuel price chart (Diesel vs. petrol, 2022–2026): Department for Energy Security and Net Zero data.

- Commodity Context / Rory Johnston Global Oil Data Deck (March 2026) – Hormuz disruption charts.

- Eurostat EU energy imports (2021–2024) and fuel price maps.

- US EIA / Bloomberg California fuel prices and West Coast refinery capacity charts.

- RAC Fuel Watch, AAA, GlobalPetrolPrices.com (real-time pump data as of late March 2026).

- BBC, Guardian, LA Times, and Reuters are reporting on Iran’s war supply impacts and refinery closures.

Data current as of March 31, 2026. Prices continue to move rapidly—check live sources for the latest. Stay tuned to Energy News Beat for ongoing coverage of the energy transition and geopolitical shocks.

What do you feel about this post?

Like

Love

Happy

Haha

Sad