We are confirming the panel discussion for next Wednesday and are excited to visit with Professor Mische and Mike Ariza on this national crisis unfolding. This article is only a warm-up for next week and is really just my show notes to get questions ready. After sitting in on a town hall with Professor Mische and Mike, I had better show up to the interview ready with questions.

How Green Energy Policies and CARB Regulations Are Gutting the State’s Oil Industry, Driving Up Imports, and Setting the Stage for $10–$15 GasolineCalifornia’s energy future is hanging by a thread.

Once a powerhouse of domestic oil production and refining, the Golden State is now “running on empty”—reliant on foreign crude, surging imports of finished fuels, and a shrinking fleet of refineries strangled by California Air Resources Board (CARB) rules, Low Carbon Fuel Standard (LCFS) mandates, cap-and-trade costs, and unique CARBOB gasoline specifications. In-state crude production has plummeted over the last 20 years, refinery closures have accelerated, and logistical bottlenecks at ports and pipelines mean the state cannot easily import its way out of trouble.

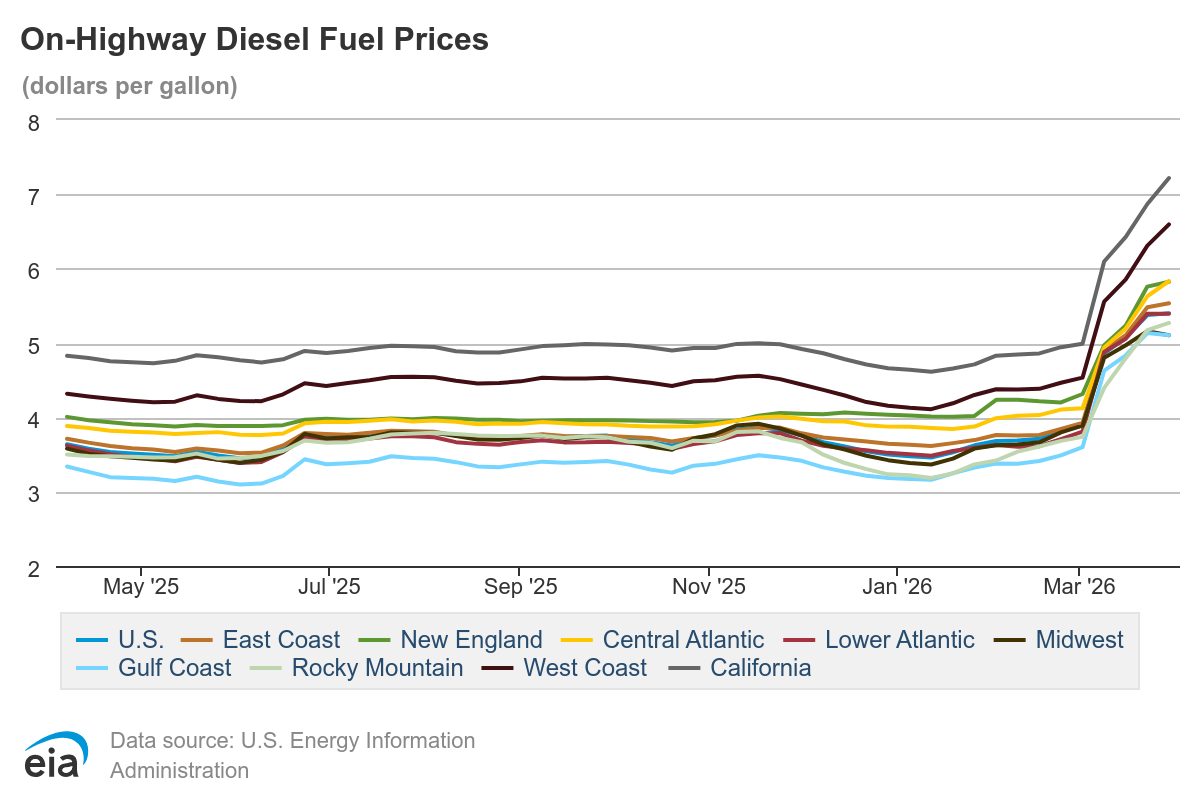

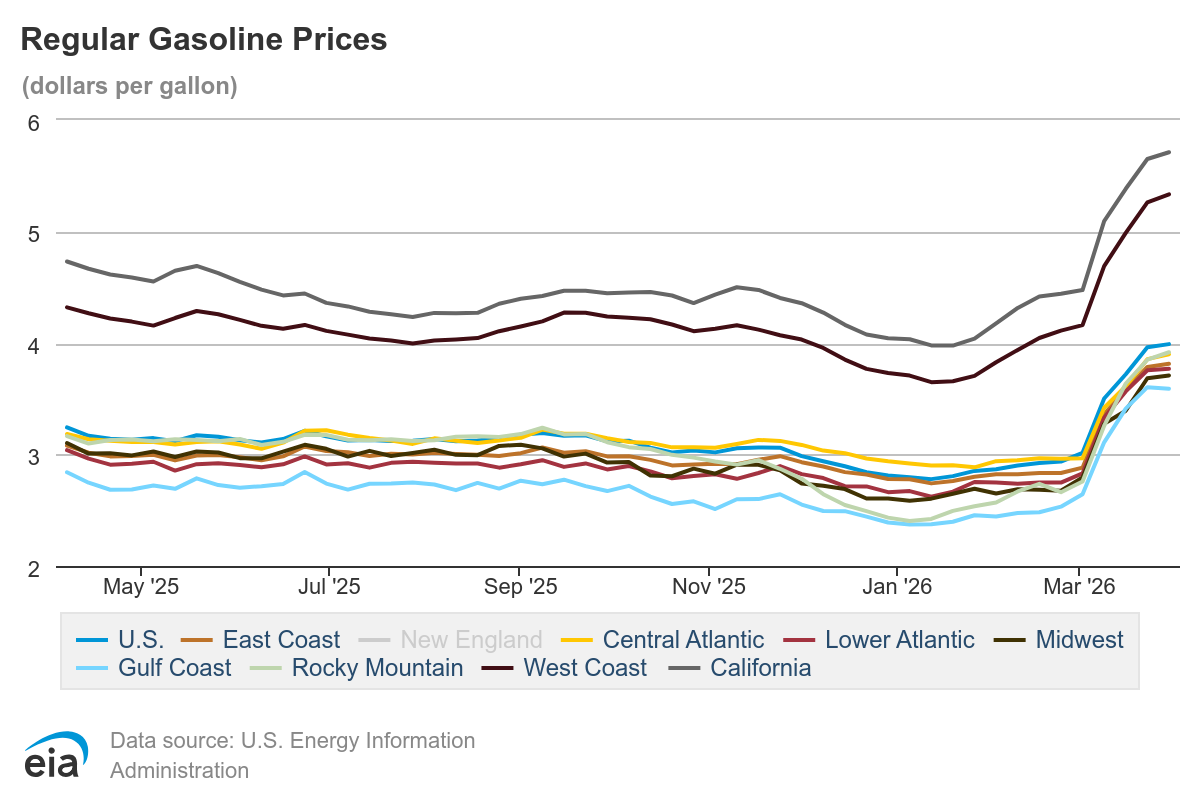

If the remaining refineries fall, analysts warn that gasoline prices could spike to $8, $10, or even $15 per gallon amid a supply shock. The solution? Federalize downstream regulatory oversight to protect what’s left of California’s refining capacity before it’s too late.

We are seeing this hit home quickly, as California is the weak link in the United States’ Energy Dominance plans. President Trump says we have all of the oil we need. Well, we need to show him the maps, and who imports the 2% for the United States that goes through the Strait of Hormuz.

What is also not discussed is the amount of diesel, gasoline, and jet fuel imported from China, South Korea, India, and other parts of Asia.

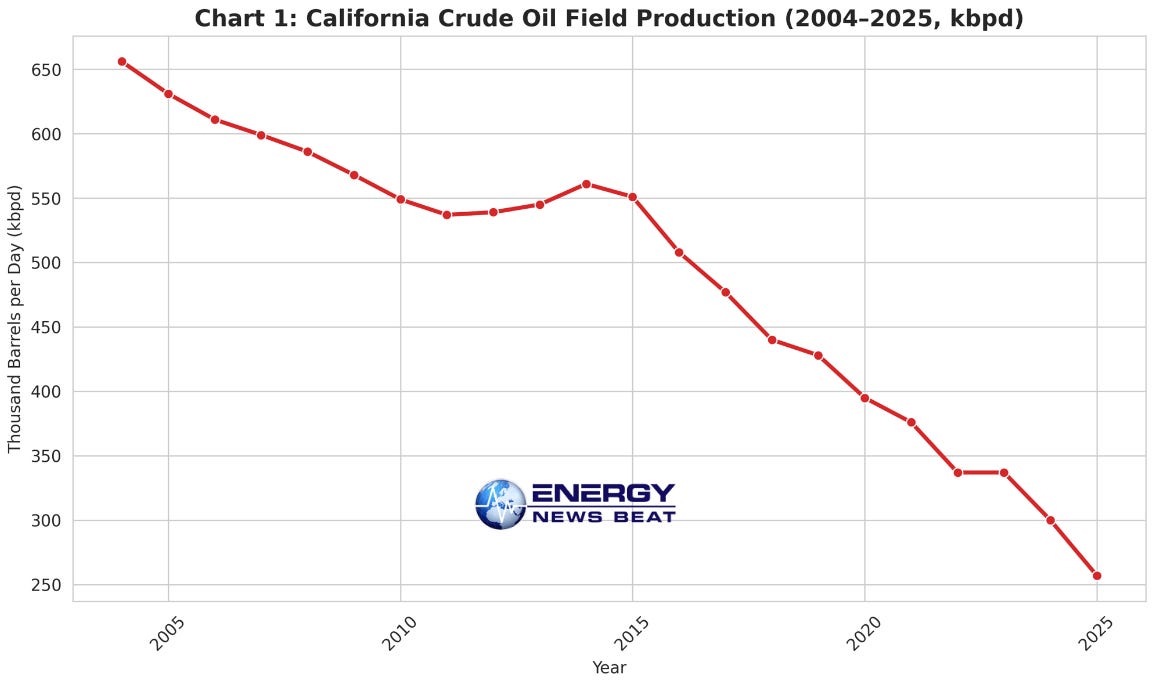

20 Years of Declining Oil Production

California’s crude oil output has been in steady freefall. According to U.S. Energy Information Administration (EIA) data, field production averaged 653 thousand barrels per day (kbpd) in 2004. By 2024, it had fallen to 296 kbpd—a drop of more than 55%.

Here’s the yearly average production (thousand barrels per day):

2004: 653

2005: 630

2010: 544

2015: 550

2020: 391

2024: 296

This decline stems from aging fields, regulatory hurdles on new drilling and permitting, and a deliberate state policy shift away from fossil fuels.

In-state crude now supplies only about 23% of refinery needs; the rest comes from Alaska (16%) and foreign sources (61%, including Brazil, Iraq, Guyana, Ecuador, and Saudi Arabia).

Chart 1: California Crude Oil Field Production (2004–2024, kbpd average)

(Line chart showing sharp decline from ~653 kbpd in 2004 to ~296 kbpd in 2024. Data source: EIA.)The trend is clear: California is producing less and less of its own oil while demand for transportation fuels remains high.

Even with Sable Offshore coming online, it is not enough to curb the closure; it will help, and it is a huge start. But that is it, a start that Gavin is trying to shut down through lawsuits.

Green Policies and CARB: The Refinery Killer

CARB’s aggressive environmental mandates—CARBOB reformulated gasoline, LCFS credits, cap-and-trade, and ever-tightening emissions rules—have made California refining uniquely expensive. Operating costs run 25–37% above the national average. Refiners face multimillion-dollar fines (e.g., Valero’s $82 million hit) while importers often face lighter burdens.

The result? A wave of closures and conversions. California had 23 operating refineries in 2000. That number fell to 14 by early 2024, with further drops expected. Recent and planned closures include Phillips 66’s Wilmington/Los Angeles complex (139 kbpd, closed late 2025) and Valero’s Benicia refinery (145 kbpd, closing April 2026). These alone wipe out ~17% of statewide capacity.

Today, only about 7 major gasoline-producing refineries remain operational, with multiple others signaling plans to exit or convert to renewable diesel. This matches industry warnings that the state is down to a handful of vulnerable facilities.

Imports Are Rising—But Ports and Pipelines Can’t Keep Up

As local refining shrinks, imports of finished products have surged. Gasoline imports into California averaged ~120 kbpd in 2025 (nearly double prior years), with peaks even higher. Diesel and jet fuel imports are also climbing.

Current import sources (2024–2025 data): Gasoline & blending components: Primarily Asia (India, South Korea, Taiwan ~2/3 of volume), with growing volumes rerouted via the Bahamas to comply with the Jones Act for U.S.-origin product.

Jet fuel: Heavily from South Korea, with contributions from China and others; West Coast imports hit record levels post-closures.

Diesel: Similar Asian sources plus limited domestic reroutes.

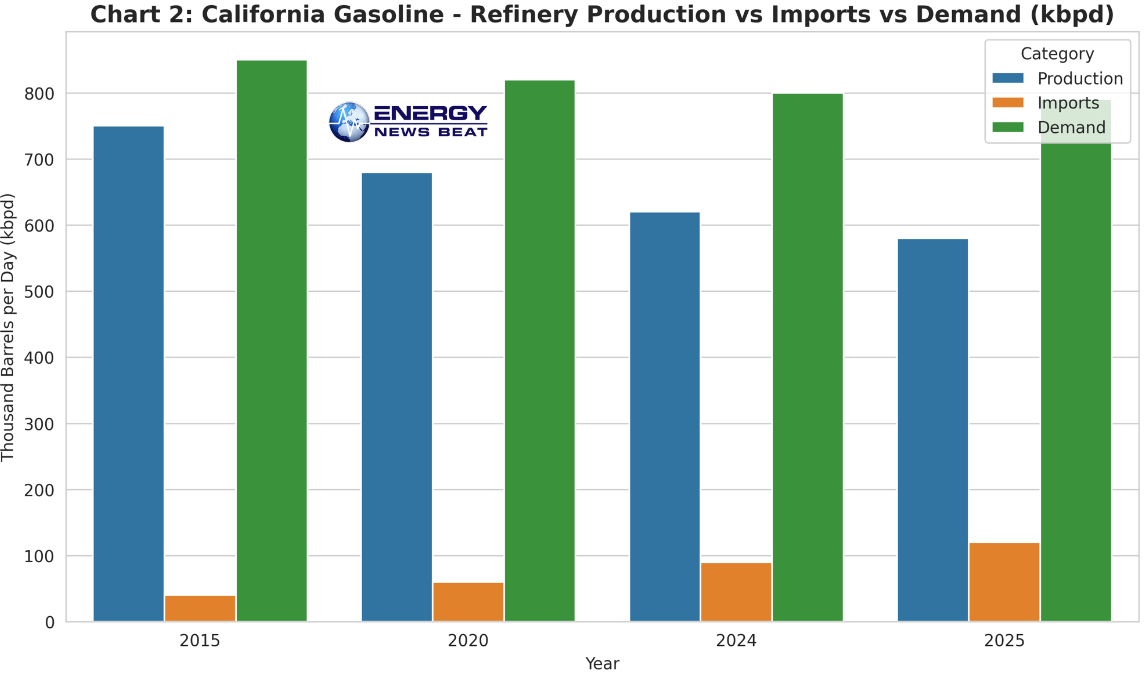

California Gasoline – In-State Refinery Production vs. Imports vs. Demand (recent trend, kbpd)

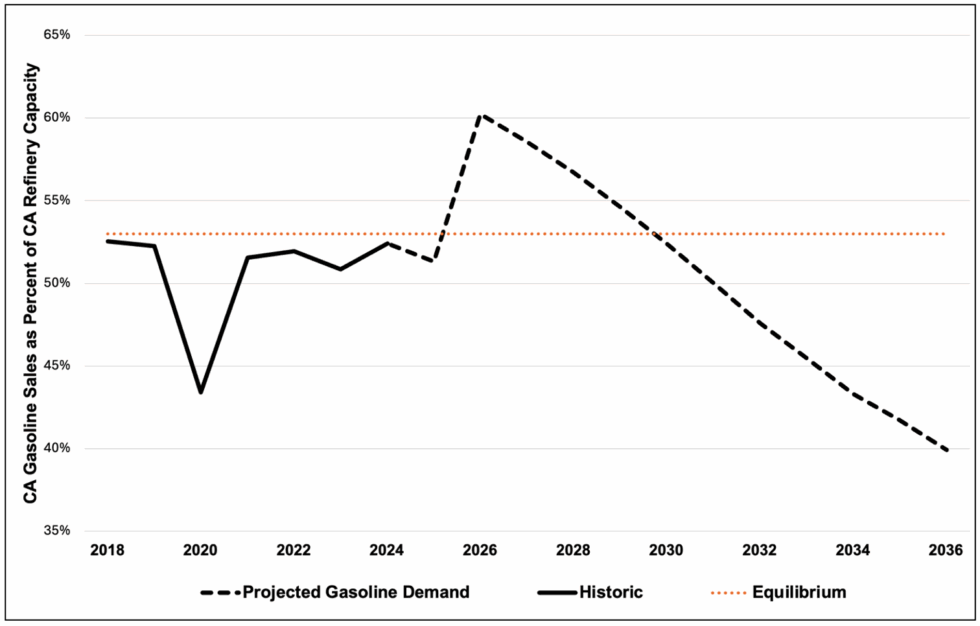

The problem is in their reporting and ideological stance. The following chart is from Stillwater Analysis of EIA California Crude Capacity vs CARB LCFS Gasoline Volumes. They are still operating in a delusional dream that gasoline demand is going away and everyone will be walking or driving an EV.

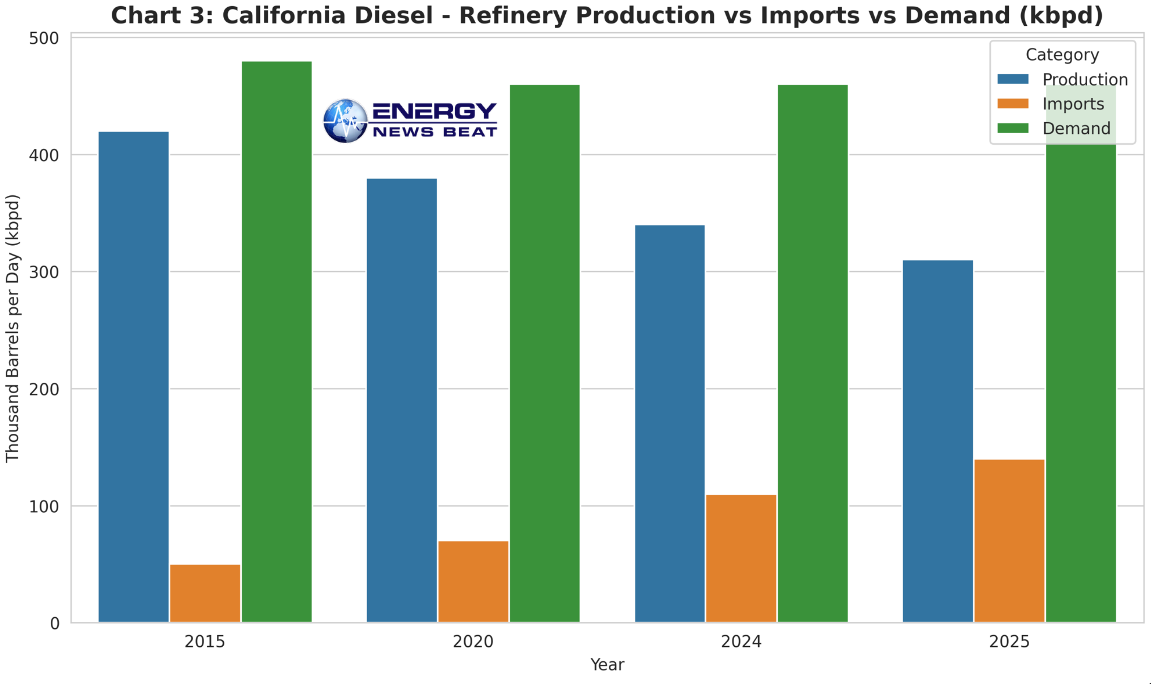

Chart 3: California Diesel – In-State Production vs. Imports vs. Demand (kbpd)

(Similar pattern: Demand steady/growing with renewable diesel blend; fossil diesel imports increasing as refineries close.)

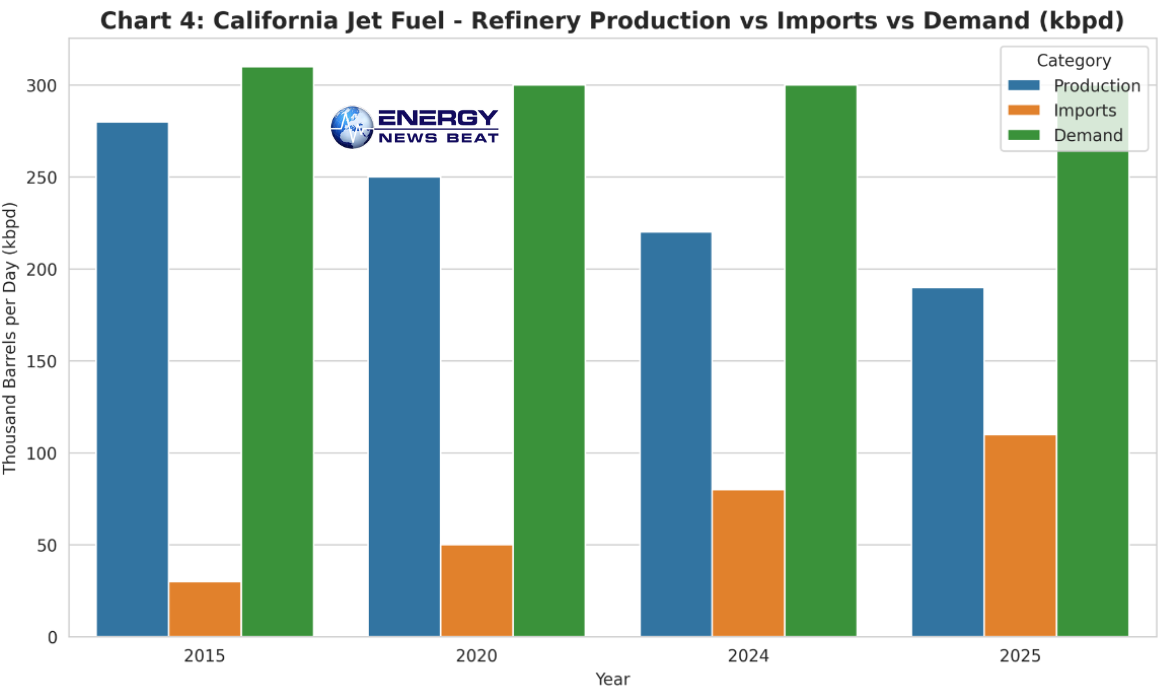

Chart 4: California Jet Fuel – In-State Production vs. Imports vs. Demand (kbpd)

(Demand high as #1 U.S. state consumer; local refinery output falling; imports from Asia filling 15–20%+ of needs, with military bases heavily dependent.)

This is the one that should get our Secretary of War fired up. Just saying, try defending the West Coast with no Jet Fuel.

Terminal and pipeline capacity for clean products is limited—practical sustainable imports top out well below theoretical maxima due to congestion, weather, and competition among products.

Jones Act requirements further complicate and increase the cost of domestic-origin fuel. Getting the Jones Act repealed will help import from US refineries, but they will still be put on tankers and shipped through the Panama Canal. Adding costs that don’t need to be there.

Exports Are Already Being Limited—$10–$15 Gas Is Closer Than You Think

The financial impact would be catastrophic: higher costs for everything from commuting and freight to goods and services, hitting low- and middle-income families hardest while accelerating the very economic pain green policies claim to avoid.

The Fix: Federalize Downstream Regulatory Issues Now

California cannot regulate itself into an energy crisis and then expect the rest of America to bail it out with tankers and higher prices. It’s time to save the refineries that still power the state.

If California fails, Mike Umbro is right. This will be a blight on President Trump’s financial record. Mike Ariza is also spot on, and the National Security risk Gavin Newsom has created has the potential to bring the Republic down entirely.

I am really looking forward to the California Running on Empty panel next week with David Blackmon, Mike Ariza, and Professor Mische. Let me know if you like my show notes. I’m getting ready for the podcast.

Also, a shout-out to our great Sponsors:

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast

https://reeseenergyconsulting.com/.

A shout-out to our New Sponsor, Data2 – We will be running an AI Centered Series and have lots of data rolling out!. https://www.data2.ai/resources/the-decision-lag-report

And we have WellDatabase rolling in as a new sponsor, and we will be getting their information next week.