As the Iran war enters its fifth week and the Strait of Hormuz remains effectively closed, Goldman Sachs has issued a stark warning in its April 2026 report titled “Are We Running Out of Oil?”

The bank’s analysts, led by Yulia Zhestkova Grigsby, conclude that the world is indeed facing acute physical shortages of crude and refined products—the largest supply shock in history. While global oil reserves exist, logistics breakdowns, depleted tanker flows, and critically low regional stockpiles are triggering cascading shortages, price spikes, and the early stages of rationing, particularly in Asia.

We are not running out of oil; rather, we are living through the misinvestment in wind, solar, and hydrogen, with minimal exploration and production or pipeline development. All to avoid the Net Zero crisis we have been warned about for decades, which has disappeared when the Strait of Hormuz was shut down for 30 days. The oil glut narrative has also seemed to disappear. We are witnessing in real time that the world moves on oil, and gas, and our food supply is in jeopardy with the disruption not of wind and solar, but the disruption of oil and gas.

The report builds on earlier Goldman forecasts (raised in March 2026) that lifted 2026 Brent crude averages to $85 per barrel (from $77) due to prolonged Hormuz disruptions. It now drills into product-specific and country-level tightness, warning that if Gulf flows stay near zero, “outright supply rationing becomes inevitable.”

The Scale of the DisruptionGoldman Sachs reports a 94% collapse in daily shipping flows through the Strait of Hormuz compared to pre-war levels. Middle East oil and refined product exports have plunged 63%, from 7.4 million to 2.8 million barrels per day. Refined products have been hit even harder:

Fuel oil: –88%

Jet fuel: –85%

Naphtha: –73%

LPG: –65%

Diesel: –55% (largest absolute volume loss)

Asia, which accounts for one-third of global refined products demand and relies on the Persian Gulf for roughly half its supply, faces the most severe exposure. Western nations are less immediately impacted but will feel secondary effects through soaring global prices and diverted cargoes.

Product-by-Product Shocks

Diesel: The hardest-hit product in volume terms. Critical for trucking, shipping, agriculture, and industry. Prices have already skyrocketed in many regions. Singapore, Taiwan, and South Korea face near-total loss of Gulf diesel inputs; other Asian economies are severely affected. Europe and the U.S. will see price contagion but lower direct volume losses.

Gasoline: Similar patterns to diesel, though slightly less severe in some Asian markets. Demand destruction (reduced driving) is expected in price-sensitive regions as pump prices surge.

Jet Fuel: Aviation is highly exposed. India and South Korea have lost 100% of Gulf supplies; Japan, Taiwan, and China are also badly hit. The UK faces a 41% loss outside Asia. Specialized storage means reserves are limited, already forcing airport advisories (e.g., limited supplies in Italy).

Naphtha & LPG: Naphtha (key plastics/petrochemical feedstock) shortages are shutting Indian plants. LPG (used for cooking and heating in Asia) losses are acute for Japan, South Korea, India, and especially Singapore (total loss).

Fuel Oil: Globally the most vulnerable. Seven Asian nations are 100% dependent on Gulf supplies; the U.S. is ~60% exposed. Singapore is uniquely vulnerable across all products.

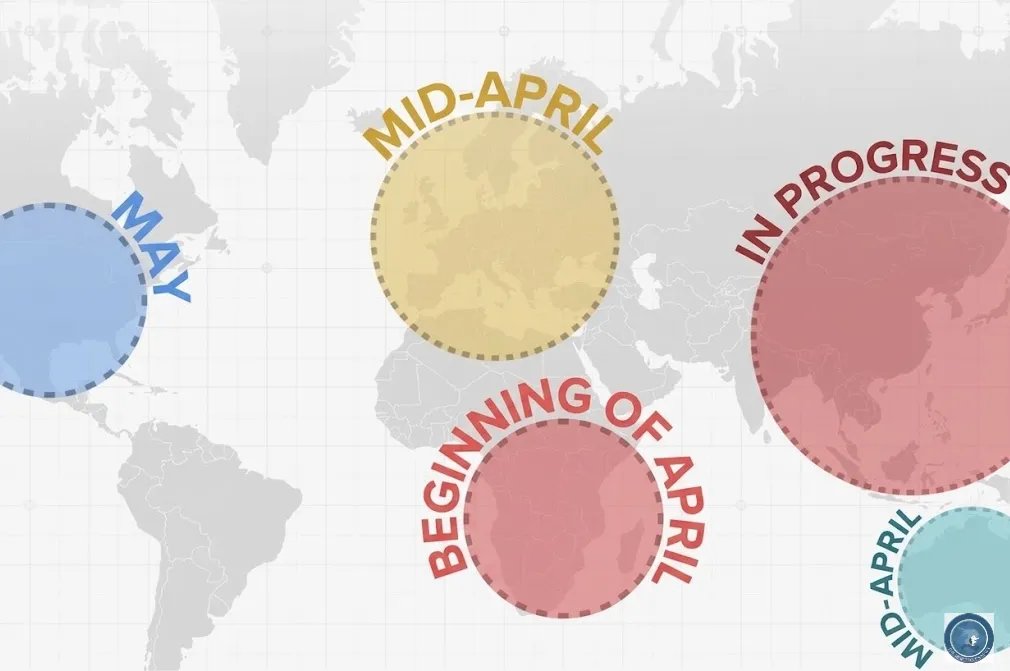

Rationing Timelines by Major Region

Goldman and complementary JP Morgan analysis highlight that strategic stocks average ~40 days of crude and ~37 days of refined products globally—but many Asian nations are far lower (India: 16 days refined; Thailand: 17 days crude).

The last pre-war Gulf tankers are arriving now, with shortages spreading east-to-west.

Asia (already in crisis – March/April 2026 onward)

Shortages hit first here. Many countries have implemented or announced rationing:

Fuel caps, odd-even driving rules, shortened work/school weeks (4-day weeks in Sri Lanka, Myanmar), export bans on fuels (China), and emergency conservation orders.

Affected nations include South Korea, Singapore, Thailand, India, the Philippines, Pakistan, Bangladesh, Vietnam, Indonesia, Cambodia, and Sri Lanka.

Panic buying and queues reported in China; plastics and petrochemical plants shutting.

Europe (April 2026 onward – shortages imminent)

Last Gulf tankers (including jet fuel) due around early April. Shell CEO warned Europe faces fuel shortages “as soon as next month” without reopening. Diesel pressure is expected next, followed by gasoline in the summer driving season. Slovenia has already introduced formal rationing (50 liters/week for private drivers). Italy airports are limiting jet fuel. Broader EU measures (hoarding curbs, potential caps) are under discussion as diesel and jet fuel tighten.

United States & Americas (late April/May 2026 onward – price-driven impacts dominant)

U.S. faces 60% fuel oil exposure but benefits from domestic production and record refined product exports (3.11 mb/d in March) to Asia/Europe. Gasoline and diesel prices have risen sharply (35% for gasoline since early March). Formal rationing is not yet widespread, but Goldman warns of “significant price-driven demand destruction” in flexible-price markets. Latin America faces similar secondary pressures.

If Hormuz flows remain near zero beyond the next few weeks, Goldman states no further offsets are available and physical rationing will spread. Demand destruction (flight cuts, factory shutdowns, reduced driving) and job losses (e.g., European trucking) are already materializing.

Outlook and Broader ImplicationsGoldman’s base case assumes limited recovery, but risks remain skewed higher if infrastructure damage persists (Qatar LNG repairs could take up to 5 years). The shock is already raising recession odds (Goldman now at 30% for the U.S.) and inflation forecasts.

For energy markets, the message is clear: this is not just a price story—it is a physical availability crisis rolling out region by region. Policymakers are shifting from price mitigation to conservation and rationing. Consumers and businesses should prepare for sustained higher costs and potential supply constraints into the summer and beyond.

- X Thread by

@ChrisO_wiki

summarizing Goldman Sachs report (posted April 5, 2026): https://x.com/ChrisO_wiki/status/2040708045487985104

- Goldman Sachs Research: “Are We Running Out of Oil?” (April 2026) – Yulia Zhestkova Grigsby, Alexandra Paulus, Daan Struyven et al. (cited in thread).

- Bloomberg: “Goldman Sachs Raises Oil Forecasts on Largest-Ever Supply Shock” (March 23, 2026): https://www.bloomberg.com/news/articles/2026-03-23/goldman-sachs-raises-oil-forecasts-on-largest-ever-supply-shock

- Reuters / various: U.S. fuel export records, rationing measures in Asia/Europe (March–April 2026 reports).

- JP Morgan “ticking time bomb” map and analysis (referenced in thread; March 2026): coverage at https://www.morningstar.com/news/marketwatch/20260326489/this-map-shows-a-crude-ticking-time-bomb-that-hits-much-of-the-worlds-oil-supply-in-april

- Additional reporting: CNBC, The Guardian, Reuters, Forbes on country-specific rationing and Shell CEO comments (March 25–April 5, 2026).

- EU Energy Commissioner statements on persistent tightness (April 1, 2026).

All data current as of April 5, 2026. Energy News Beat will continue monitoring developments.