The Iran war has delivered the largest supply shock in energy-market history, with Gulf producers shutting in roughly 9 million barrels per day (bpd) of crude and related liquids. While a potential two-week ceasefire has sparked some price relief, analysts and the U.S. Energy Information Administration (EIA) agree that full market stabilization will take months — not weeks — because of shipping backlogs, damaged infrastructure, and lingering insurance and confidence issues in the Strait of Hormuz. Even after flows resume, a structural risk premium will keep the new oil-price floor around $82 per barrel for Brent crude through the balance of 2026.

The Scale of the Shut-Ins: 9.1 Million Barrels per Day in April

According to the EIA’s April Short-Term Energy Outlook:

March 2026: Iraq, Saudi Arabia, Kuwait, UAE, Qatar, and Bahrain collectively shut in 7.5 million bpd of crude.

April 2026: The figure rises to a peak of 9.1 million bpd — equivalent to nearly 10% of global oil supply.

May onward (assuming ceasefire by end-April): Shut-ins ease to 6.7 million bpd, with a slow ramp-back to pre-war levels only by late 2026.

This is on top of the near-total paralysis of the Strait of Hormuz, which normally carries ~20% of global seaborne oil and LNG. The International Energy Agency (IEA) has labeled it “the largest supply disruption in the history of the global oil market.”

Refining Capacity Hit: ~2 Million Barrels per Day Offline

Physical attacks and precautionary shutdowns have idled 1.9–2.35 million bpd of Gulf refining capacity (per IIR and Reuters estimates). Key facilities affected include:

Saudi Aramco’s Ras Tanura (550,000 bpd) — temporarily halted, partial restart reported.

UAE’s Ruwais complex — fires and precautionary closure.

Bahrain’s Bapco Energies (400,000 bpd) — force majeure declared after damage.

Additional outages in Iraq, Kuwait, Qatar and other Saudi sites.

Downstream product markets (gasoline, diesel, jet fuel) are tightening faster than crude in some regions, amplifying the pain for importers in Asia and Europe.

LNG Shock: 12.8 Million Tonnes per Annum (MTPA) Destroyed for Years

Iranian strikes on Qatar’s Ras Laffan Industrial City knocked out two LNG trains, removing 12.8 MTPA — or 17% of Qatar’s total LNG capacity. QatarEnergy CEO Saad al-Kaabi confirmed repairs will take 3–5 years due to critical turbine and heat-exchanger shortages. This single event has:

Triggered force majeure on long-term contracts to China, South Korea, Italy, and Belgium.

Removed the equivalent of ~3–4 LNG cargoes per day from global trade.

Pushed Asian and European spot LNG prices up sharply (some sessions +35%).

Qatar normally supplies ~20% of world LNG; the outage has tightened the market for the foreseeable future.

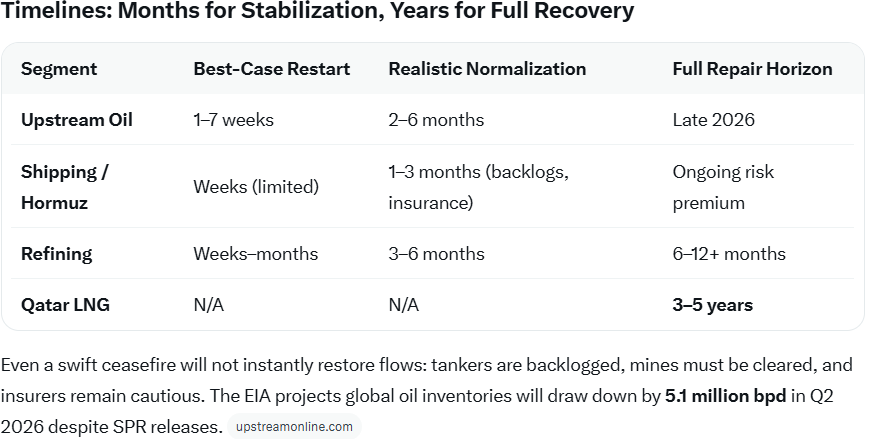

Even a swift ceasefire will not instantly restore flows: tankers are backlogged, mines must be cleared, and insurers remain cautious. The EIA projects global oil inventories will draw down by 5.1 million bpd in Q2 2026 despite SPR releases.

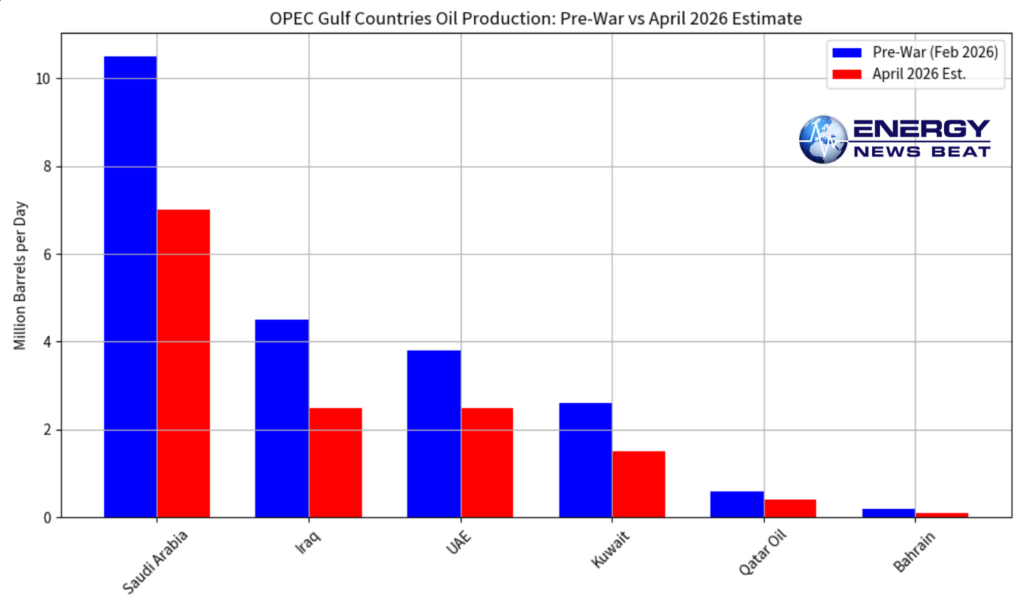

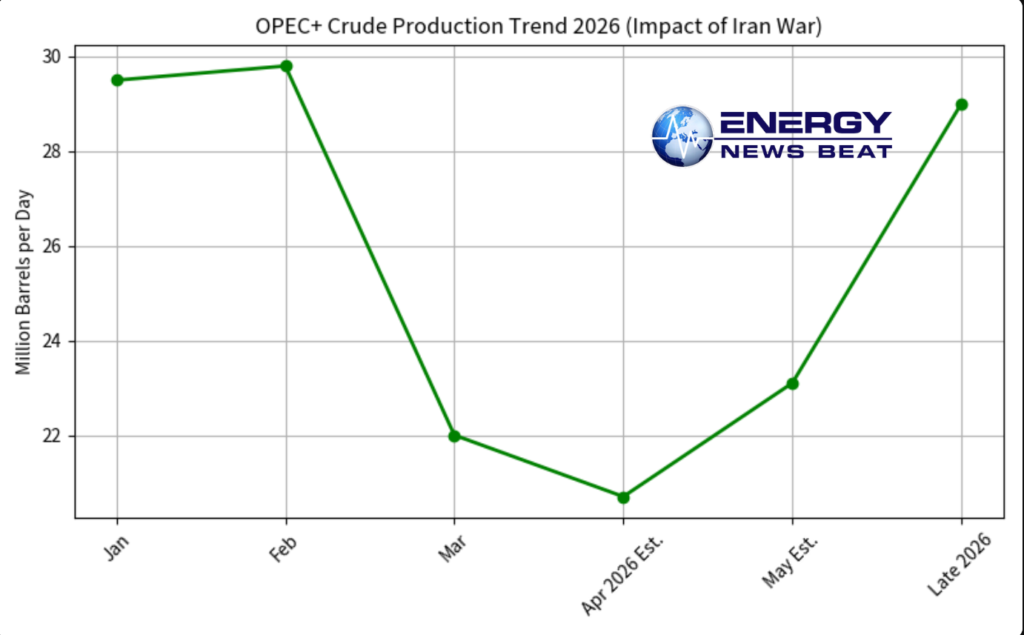

OPEC Production Charts: Pre-War vs. Current Reality

Chart 2: Gulf OPEC Countries Oil Production (Million bpd)

Chart 3: OPEC+ Crude Production Trend 2026 (Million bpd)

The charts illustrate the sudden ~9 million bpd drop and the slow multi-month climb back toward pre-war levels.

Price Outlook: $82 Becomes the New Floor

Brent crude has traded above $110 in recent weeks but eased on ceasefire talks. Forward curves and analyst consensus (EIA $96 average for 2026 Brent) now embed a persistent $10–15/bbl risk premium. Multiple houses see $82 as the new technical and fundamental floor once initial panic subsides and partial Gulf supply returns — well above the pre-war $60–70 range. Higher prices will incentivize U.S. shale, Canadian oil sands, and non-OPEC growth, but the structural Middle East premium is here to stay.

Bottom Line

The Iran war has removed ~9.1 million bpd of oil, ~2 million bpd of refining, and 12.8 MTPA of LNG for years. Shipping and confidence will take months to normalize; full LNG repairs will take years. Markets are already pricing in a higher-for-longer regime, with $82/bbl emerging as the new oil-price floor. Investors should watch:

Ceasefire durability and Hormuz reopenings.

Weekly tanker transit counts.

EIA/IEA inventory draws.

Any acceleration of U.S. or Brazilian non-OPEC supply.

Energy markets have entered a new, more volatile chapter — one where geopolitics, not just economics, sets the floor.

Energy News Beat – Independent energy market analysis. All data as of April 8, 2026.

- Bloomberg / EIA: “Mideast Oil Output Seen Dropping by 9 Million Barrels a Day” (April 7–8, 2026) – https://www.bloomberg.com/news/articles/2026-04-07/mideast-crude-output-seen-dropping-by-9-million-barrels-a-day

- U.S. EIA Short-Term Energy Outlook (April 2026) – https://www.eia.gov/outlooks/steo/report/global_oil.php

- Reuters: “Iran attacks wipe out 17% of Qatar’s LNG capacity for up to five years” (March 19–20, 2026) – https://www.reuters.com/business/energy/iran-attack-damage-wipes-out-17-qatars-lng-capacity-three-five-years-qatarenergy-2026-03-19/

- Insurance Journal: “List of Gulf Energy Infrastructure Damaged in Iran War” (April 7, 2026) – https://www.insurancejournal.com/news/international/2026/04/07/864740.htm

- IEA Oil Market Report – March 2026 – https://www.iea.org/reports/oil-market-report-march-2026

- Argus Media / Upstream Online: Refining and OPEC+ updates (March–April 2026)

- Rystad Energy: Qatar LNG repair timelines (March 25, 2026)

All figures cross-referenced from EIA, IEA, Reuters, and Bloomberg reporting.