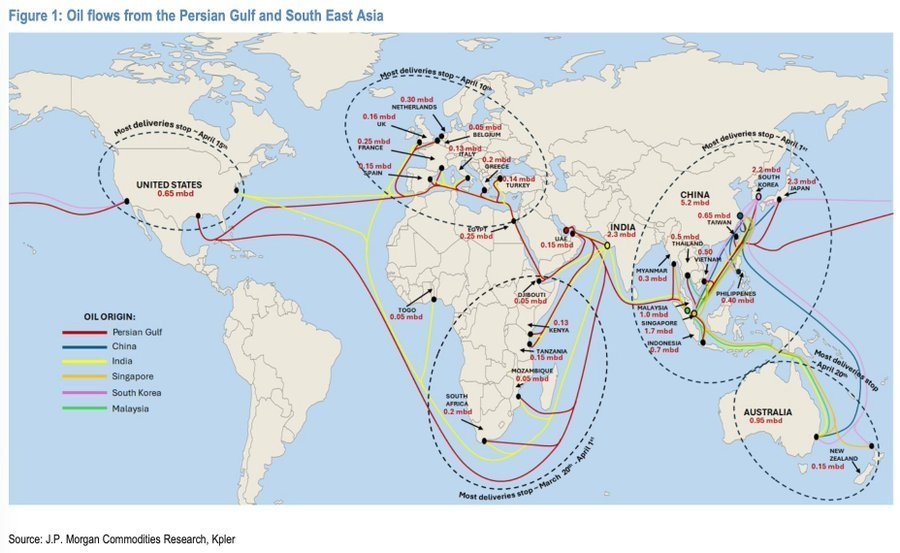

The Strait of Hormuz remains effectively closed amid the ongoing U.S.-Israel conflict with Iran, halting nearly all tanker traffic through the critical chokepoint that normally carries about 20% of global oil and LNG trade, along with roughly 5 million barrels per day (mbd) of refined petroleum products. JP Morgan Commodities Research has modeled the ripple effects, highlighting how existing in-transit cargoes will deplete at different rates around the world based on voyage times. A widely circulated map from their analysis (shared on X by @pplsartofwar) illustrates oil flows from the Persian Gulf and projects when “most deliveries stop” for major importing regions.

Regional Timelines for Supply Disruptions (Crude Oil Flows)The JP Morgan map (sourced from Kpler data) traces Persian Gulf oil routes in red and overlays dashed circles showing depletion timelines for pre-closure cargoes:Asia: Most deliveries stop April 1, 2026. This includes major importers like China (5.2 mbd), India (2.3 mbd), Japan, South Korea, and Southeast Asian nations. Proximity means Asia feels the pinch first and hardest—90% of Hormuz exports are destined here.

Europe: Most deliveries stop April 10, 2026. Flows to the UK, Netherlands, France, Spain, Italy, and others (totaling hundreds of thousands of bpd) will taper off next.

North America (primarily U.S.): Most deliveries stop April 15, 2026. U.S. imports from the region (0.85 mbd shown) are smaller but still significant for certain grades.

Australia (and New Zealand): Most deliveries stop April 20, 2026. Australia (0.95 mbd) sits at the end of the supply chain, making it the last major region affected.

These dates assume no resumption of flows and factor in sailing times from the Gulf. Earlier JP Morgan notes (mid-March) already flagged that Asia-bound supplies could run dry “this week” and Europe-bound next, with the April projections reflecting full inventory drawdowns.

Product-Specific Impacts: Diesel, Gasoline, Jet Fuel, Naphtha, and Others

While crude dominates headlines, JP Morgan emphasizes that the Strait is a major artery for refined products—roughly 5 mbd pre-crisis. The closure has already triggered refinery outages (up to 2 mbd in the Middle East) and production shut-ins (now approaching 6.5–12 mbd globally, creating a 6–7 mbd supply deficit below demand). Shortages are acute in middle distillates and petrochemical feedstocks.

Key product breakdowns and regional effects (per JP Morgan and related analysis):

Diesel: Europe is particularly exposed, sourcing about one-third of its diesel imports from the Gulf. Shortages here could hit trucking, agriculture, and heating, exacerbating post-Russian import ban vulnerabilities. Global diesel markets are already seeing sharp tightness.

Jet Fuel (Aviation Fuel): Europe again relies heavily on Middle East exports (one-third of imports). Asia is also vulnerable. Rising prices have already triggered flight cancellations in affected regions; JP Morgan notes this as a high-impact area alongside diesel.

Naphtha: One of the hardest-hit products. Critical for petrochemicals (plastics, ethylene, etc.), it heavily affects Asia’s industrial and manufacturing sectors. Disruptions ripple into fertilizers, packaging, and autos. JP Morgan flags naphtha, LPG, and jet fuel as seeing “particularly severe” impacts.

LPG (Liquefied Petroleum Gas): Major shortages noted globally, affecting heating, cooking, and petrochemical feedstocks—especially in Asia and parts of Europe.

Gasoline and Other Petroleum Products:

Less emphasized in JP Morgan’s product alerts than distillates, but still part of the 5 mbd refined flow. Broader crude deficits will pressure gasoline blends indirectly, though U.S. domestic production offers some buffer.

Overall Crude: Global supply losses projected at 8–12 mbd in the coming weeks, with Middle East benchmarks (Dubai/Oman) spiking far higher than Atlantic ones (Brent/WTI) due to geographic dislocation.

Asia is bearing the initial brunt of refined products (imports down 35% in some less-wealthy countries, prompting demand curbs like four-day workweeks). Europe faces middle-distillate pain. North America and Australia have longer buffers, but are not immune. Even if the Strait reopens quickly, JP Morgan warns of lingering “supply-chain air pockets” and elevated prices.

Broader Implications

JP Morgan’s analysis underscores that this is more than a crude story—it’s a sequenced shock to global supply chains. Storage in the Gulf is filling rapidly, forcing upstream shut-ins (already at 6.5+ mbd). Strategic reserves and alternative routes (e.g., limited pipeline or Red Sea workarounds) offer only partial relief. Prices have already pushed Brent above $100–110/bbl in recent trading, with potential for further spikes if the closure persists.

Energy News Beat will continue monitoring developments, including any de-escalation signals or SPR releases. For now, the JP Morgan map serves as a clear visual timeline: the world is entering a phased energy crunch, starting in Asia next week and spreading westward through April.

Appendix: Sources and Links

The article was based on the JP Morgan Commodities Research analysis (via Kpler shipping data) that was widely shared and summarized in public reporting. Below is a complete list of primary sources and direct links used for the regional timelines, product-specific impacts, supply-cut estimates, and map details:

- X Post by

@pplsartofwar

(March 27, 2026) – Direct share of the JP Morgan / Kpler map showing Persian Gulf oil flows and depletion timelines (Asia: April 1; Europe: April 10; North America: April 15; Australia: April 20). Includes the original map graphic.

Link: https://x.com/pplsartofwar/status/2037611169645486186 - Reuters – “JP Morgan sees crude supply cuts nearing 12 million bpd as tanker halt tightens” (March 13, 2026) – Details Asia/Europe flow depletion timelines, production shut-ins (6.5+ mbd), and refined-product shortages (diesel, jet fuel, LPG, naphtha).

Link: https://www.reuters.com/business/energy/jp-morgan-sees-crude-supply-cuts-nearing-12-million-bpd-tanker-halt-tightens-2026-03-13/ - MarketWatch – “This map shows a crude ticking time bomb that hits much of the world’s oil supply in April” (March 26–27, 2026) – Direct coverage of the JP Morgan map and sequential regional shock timelines.

Link: https://www.marketwatch.com/story/this-map-shows-a-crude-ticking-time-bomb-that-hits-much-of-the-worlds-oil-supply-in-april-2c058db6 - JP Morgan Asset Management – “Addressing market concerns over an extended energy disruption” (published ~March 25, 2026) – Official JP Morgan note on Gulf supply risks and product-level impacts.

Link: https://am.jpmorgan.com/wr/en/asset-management/institutional/insights/market-insights/market-updates/on-the-minds-of-investors/addressing-market-concerns-over-an-extended-energy-disruption/ - JP Morgan Private Bank – “The Middle East conflict is becoming an energy problem” (March 9, 2026) – Analysis of Hormuz disruption (20–30% of global oil/LNG) and physical supply effects.

Link: https://privatebank.jpmorgan.com/eur/en/insights/markets-and-investing/tmt/the-middle-east-conflict-is-becoming-an-energy-problem - Kpler – Multiple vessel-tracking and market reports (March 1–5, 2026) – Primary data provider for the flow map and real-time tanker data used by JP Morgan (16 mbd total petroleum flows halted; product-specific breakdowns).

Key reports: - Additional JP Morgan–quoted coverage on product impacts

- Energy News / Offshore Energy: JP Morgan on diesel, jet fuel, LPG, and naphtha deficits (~7 mbd below demand) – https://energynews.oedigital.com/oil-gas/2026/03/13/jp-morgan-expects-crude-oil-supply-to-drop-by-12-million-barrels-per-day-as-a-result-of-the-tanker-ban

- FutuNN: “J.P. Morgan: Disruption in the Strait of Hormuz Continues” (naphtha, LPG, jet fuel emphasis) – https://news.futunn.com/en/post/70525717/global-insights-jp-morgan-disruption-in-the-strait-of-hormuz

These sources were cross-referenced for the article’s timelines, regional breakdowns, and product-specific effects. All dates reflect the evolving situation as of late March 2026. Energy News Beat will update this appendix as new JP Morgan or Kpler notes are released.

What do you feel about this post?

Like

Love

Happy

Haha

Sad